Over long periods of time, the returns on equities not only surpassed those on all other financial assets, but were far safer and more predictable than bond returns when inflation was taken into account. – Princeton professor Jeremy Siegel from the 2014 preface to his classic book, Stocks for the Long Run

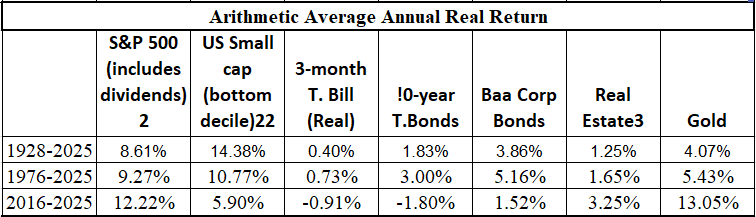

Aswath Damodaran at NYU publishes this yearly update of returns. Note that Real Estate is for Residential based on Case-Shiller data.

The typical asset allocation recommendation for portfolios of a 60/40 split between Equities and Bonds is as destructive as it is ubiquitous. Warren Buffett dealt with it in this 3 minute segment of a May 6, 2013 CNBC interview: http://video.cnbc.com/gallery/?video=3000166399 The same financial advisors will call for periodic rebalancing, as though that will compensate for 40% of your portfolio often being “dead money.” Indeed, this was even before interest rates dipped into negative territory across much of Europe, meaning you had to pay for the honor of lending your money to the government or even some companies. Some advisors will adjust the percentages based on age, others will add Cash, Commodities and/or Real Estate (REITs) as separate asset classes. Hughes Capital Management takes a much different approach.

Equities

Contrary to what many investors believe, numerous academic studies have shown that, given a sufficient investment horizon, Equities are the safest asset class. In Stocks for the Long Run, Princeton’s Jeremy Siegel points out that in the long run, bonds are riskier than stocks, despite stocks being much more volatile in the short-run. Using a data set from 1802 to 2006, Siegel found that with a 10 year horizon, the maximum loss for a capitalization weighted index of US equities was lower than the maximum loss on corporate bonds or even T-bills. At 20 years, the worst result for the index was a small gain, while both bonds and T-bills worst cases were loses. This conclusion is supported by Ken Fischer’s recent work The Little Book of Market Myths: How to Profit by Avoiding the Investing Mistakes Everyone Else Makes, which found that the long-run volatility of stocks and bonds are very similar yet historical stock returns are nearly double that of their fixed income counterparts.

The results from these two books are confirmed by the Morningstar study “Optimal Portfolios for the Long Run.” Looking at 20 countries each with 113 years of historical returns, the study constructed various portfolios based on risk aversion and time horizon. The paper found very strong evidence that a higher allocation to equities is optimal for investors with longer time horizons, and that equities become less risky over time.

As such, for investors with sufficient time horizons, Hughes Capital Management considers equities to be the bedrock of most portfolios.

Bonds

Whether Bonds should be incorporated into a fully diversified portfolio depends largely on their current yields and the broader interest rate environment. During the 2010s, the extremely low yields on Bonds meant they represented: “return-free risk.” After the more recent rise in interest rates after the COVID pandemic, funds that specialize in Bonds (both Government and Corporate) can be a useful tool to help mitigate risk. Shorter-term bond funds can also provide a place to park cash while waiting for Equity-based investment opportunities to emerge.

Cash

Cash that isn’t invested in a cash-equivalent such as a treasuries (or a fund invested in those securities) is “dead money” that should be avoided unless needed in the immediate future. It is important to note that some brokerage firms adopt a strategy of creating excess cash in a client’s portfolio, paying the client a much lower yield than market rates and pocketing the difference between “risk-free” treasuries and the client’s lower yield.

Real Estate

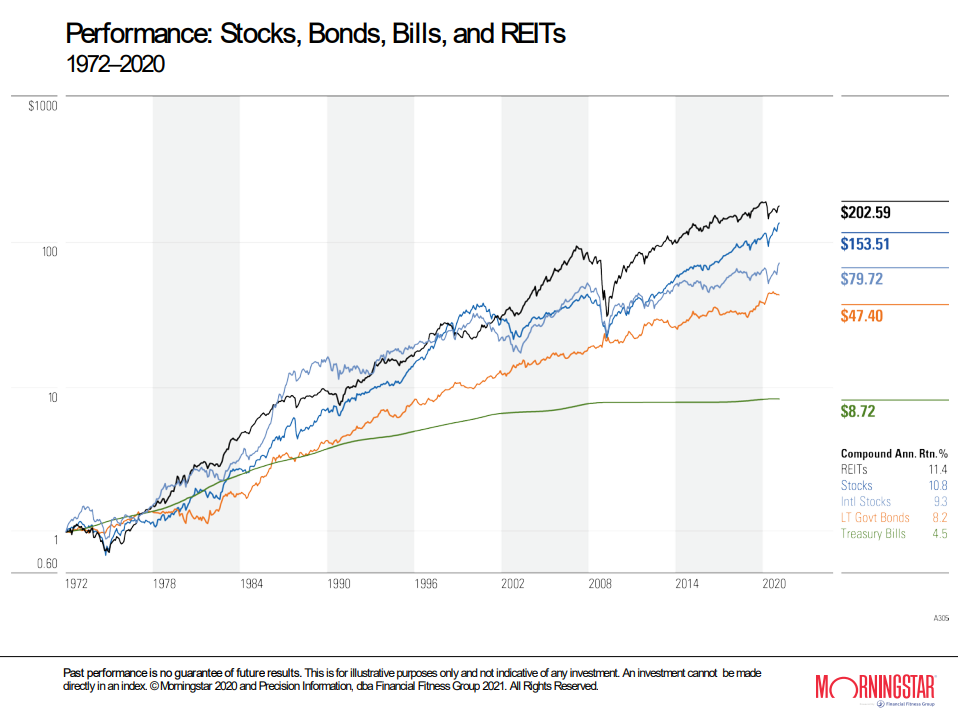

Real Estate exposure can be a critical component of a well-diversified portfolio. The best way to obtain exposure to this market is through REITs, which over the past 48 years have outperformed the broader equity market.

While the short-term volatility of REITs can be jarring (as the Great Recession in 2008 demonstrated), with a long time horizon their risk profile dramatically improves. The Morningstar graph below illustrates the realized gains and losses in REITs for one-, five-, and 15-year periods. Of the 42 one-year periods from 1972 to 2013, only eight resulted in a loss. By increasing the holding period to five years, only one of the 38 overlapping five-year periods resulted in a loss, while none of the 28 overlapping 15-year periods from 1972 to 2013 resulted in losses.

Commodities

Many investment advisors recommend a significant allocation to commodities for returns uncorrelated with the rest of the market. And while the returns from the asset class are indeed uncorrelated, for the past few decades the roll yield on many commodity futures contracts have been negative, meaning investing in these contracts has been a losing game.

In a 9/1/16 interview titled “Why Investing in Commodities Can Be Challenging”, Morningstar’s Bri